The Winning Liquidity Strategy For Pre-IPO Technology

The shift is structural, not cyclical

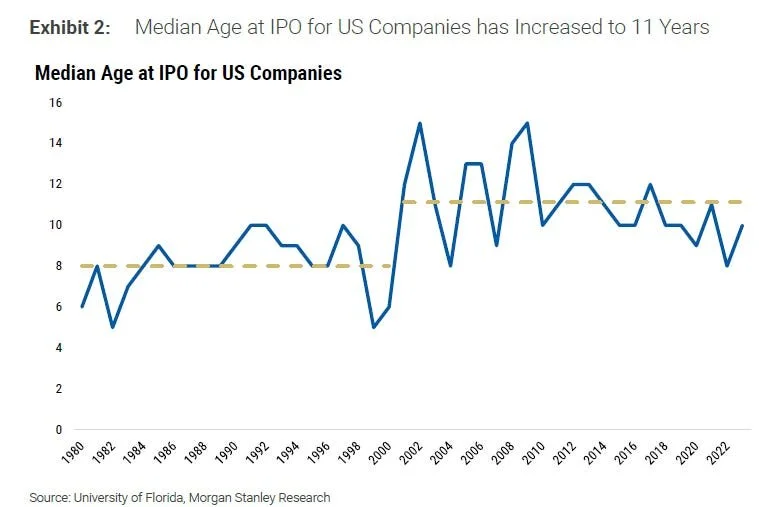

Over the past decade, private markets have undergone a structural change in how and when liquidity is realized. To repeat a well-trodden statement; companies, once expected to reach an IPO or strategic sale within a predictable timeframe, are now remaining private for significantly longer. This is not simply the result of one weak IPO year or a temporary macro shock. It reflects a higher bar for public market readiness, more selective acquirers, and a broader reassessment of risk across capital markets.

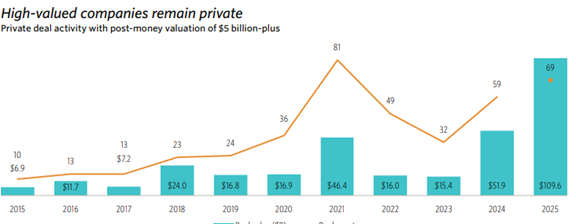

Public market access has become episodic. IPO windows open briefly, primarily reward a narrow set of companies with scale and profitability, and then close again. Technology M&A remains active but is increasingly targeted, with buyers prioritizing specific assets or capabilities, rather than broad growth-stage acquisitions. The result is a growing population of strong private companies that continue to execute well but face extended and uncertain timelines to liquidity.

When Company Maturity Outpaces Personal Liquidity

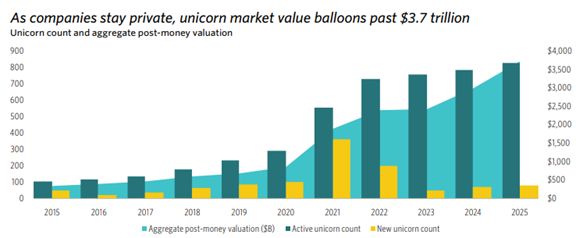

The implications of this new normal are significant, not least for those founders and teams committing much of their careers, at risk, to building outsized value. As companies mature operationally, a mismatch has increasingly emerged between business stability and personal balance sheets. It is now common to see stable growth companies with unicorn valuations, diversified revenue bases, profitable operations and professionalized governance, with founders and senior executives at incommensurate levels of personal risk – with wealth heavily concentrated in a single, illiquid asset.

This is not merely a theoretical problem, but a practical one. Equity compensation that once represented a near-term participation in value creation now often stretches over a decade or more. Over time, option exercise costs and tax liabilities can accrue well before any exit, turning what was designed as an incentive into a source of financial friction. Such delay and friction can lead to focus and motivation can be diluted, leading to less efficient companies and eventually talent leakage.

The Liquidity Options Available to Founders and Executives — and Their Trade-Offs

In the absence of a near-term IPO or acquisition, founders and senior executives typically explore a limited set of liquidity options. Each can provide partial relief, but each also carries meaningful trade-offs that boards must consider carefully.

One option is a direct secondary sale of shares. While this can provide immediate liquidity, it is often executed at a material discount to the most recent valuation, particularly in less liquid market conditions or where common shares, options or other awards are involved. Such sales can also create challenging optics with boards and investors, raising questions around confidence and alignment. From a governance perspective, uncontrolled secondary transactions risk introducing new shareholders without a clear long-term alignment to the company’s strategy.

Another nascent option is net asset value, or NAV-based, financing at the individual level. These facilities allow for borrowing against the value of shareholdings. While they avoid immediate equity sales, they typically involve personal recourse, ongoing cash-pay interest obligations, and exposure to margin or collateral calls if valuations move. With relatively few lenders willing or capable of underwriting private growth stage risk, terms can be inflexible while application to complex shareholdings can be challenging. in practice, this can add financial stress and short-term cash flow pressure, rather than reducing concentration risk.

Each of these approaches can address liquidity in isolation, but none are designed to balance the competing objectives of alignment, governance, optics, and long-term value creation.

Finding a liquidity solution that works for all is imperative if boards and investors want to maintain focus and risk appetite within the business. Liquidity, when structured carefully, buys time. It allows leadership teams to continue executing while waiting for more favourable market conditions or strategic opportunities.

Why Structured Liquidity Is Different

Pioneered by Flywheel Capital, structured growth liquidity has emerged as a deliberate third path alongside IPOs, M&A, and primary fundraising. Unlike direct secondaries or personal leverage solutions, structured growth liquidity is designed to align with the future growth of the company rather than extracting value at a point in time.

Because outcomes are tied to the company’s long-term trajectory, structured solutions can avoid the deep discounts associated with ad hoc secondary sales. They can be designed to respect existing governance, tax and incentive frameworks, limit signaling risk and ensure that liquidity supports retention and alignment rather than undermining it. For CFOs and boards, this transforms liquidity from a blunt financial event into a strategic instrument, that’s scalable across the enterprise.

Implications for Boards, CFOs, and Investors

For boards and CFOs, the central question is no longer whether liquidity should be considered, but how it can be delivered without compromising governance or long-term value creation. Structured liquidity provides a way to address real stakeholder needs while preserving strategic optionality in an uncertain exit environment.

For venture investors, introducing structured liquidity early and proactively frames it as planning rather than reaction. Positioned correctly, it becomes a tool to support portfolio company performance and retention, not a signal of distress.

The companies that navigate extended private lifecycles most effectively are those that plan for liquidity with the same discipline they apply to capital allocation.

Flywheel Capital partners with growth and late-stage companies to design structured liquidity solutions that align stakeholders, respect governance, traverse legal complexity and preserve long-term value creation.

If this could be of interest, email us at investments@flywheelcapital.io.